Abstract

This article develops a new model of business cycles. The model is economical in that it is solved with an aggregate demand–aggregate supply diagram, and the effects of shocks and policies are obtained by comparative statics. The model builds on two unconventional assumptions. First, producers and consumers meet through a matching function. Thus, the model features unemployment, which fluctuates in response to aggregate demand and supply shocks. Secondly, wealth enters the utility function, so the model allows for permanent zero-lower-bound episodes. In the model, the optimal monetary policy is to set the interest rate at the level that eliminates the unemployment gap. This optimal interest rate is computed from the prevailing unemployment gap and monetary multiplier (the effect of the nominal interest rate on the unemployment rate). If the unemployment gap is exceedingly large, monetary policy cannot eliminate it before reaching the zero lower bound, but a wealth tax can.

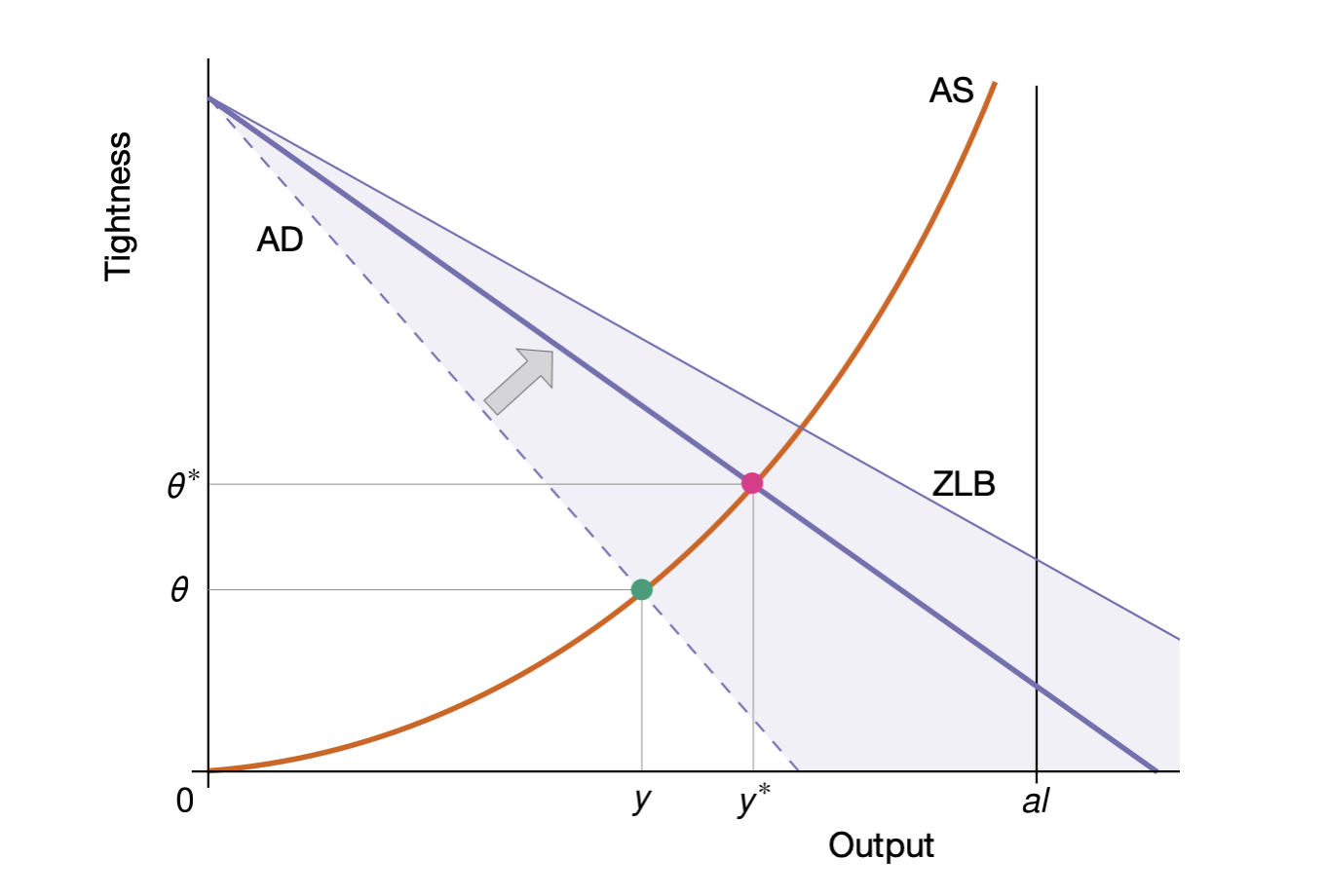

Figure 7: Optimal monetary policy under small unemployment gap

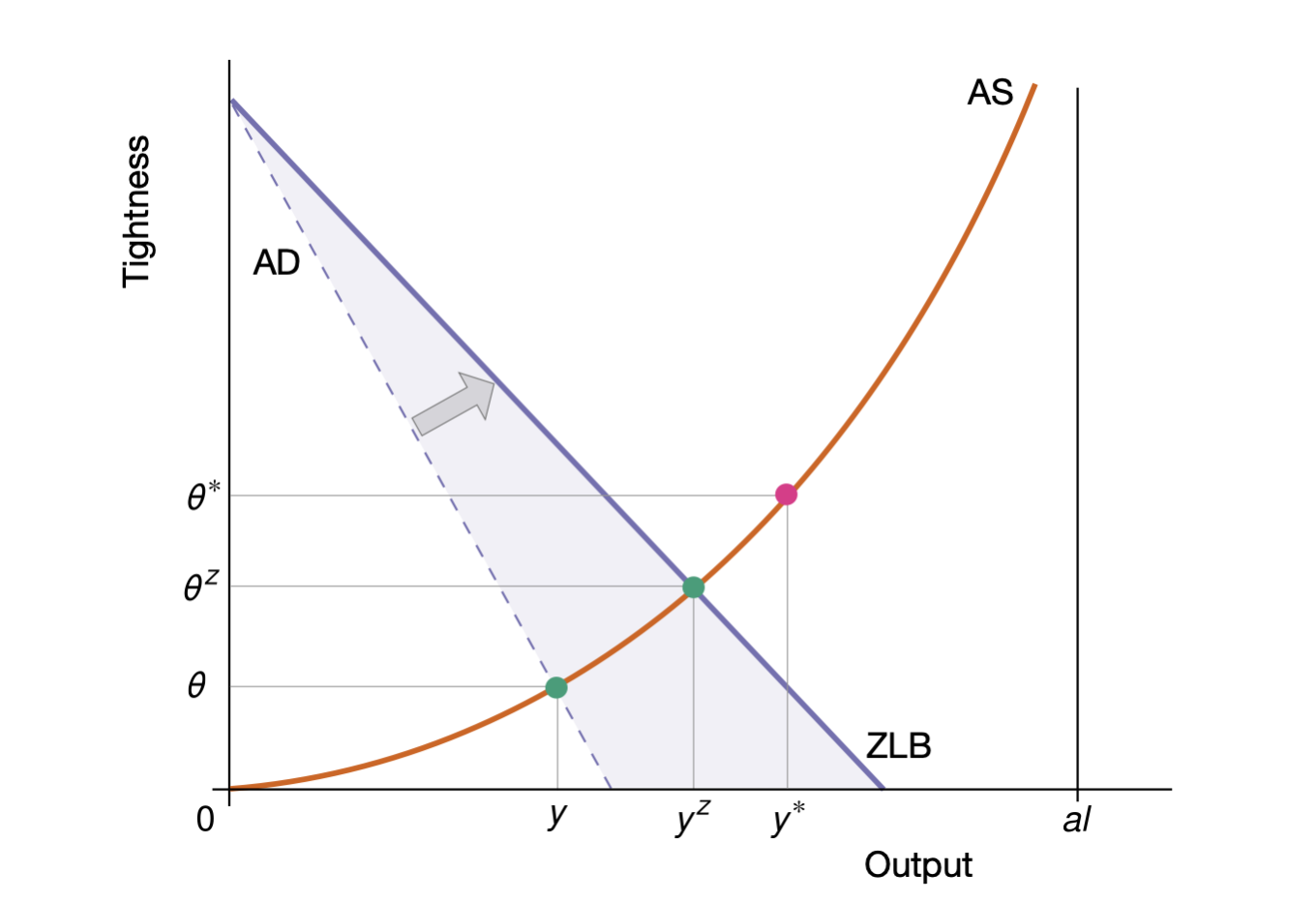

Figure 8: Zero lower bound under large unemployment gap

Citation

Michaillat, Pascal, and Emmanuel Saez. 2022. “An Economical Business-Cycle Model.” Oxford Economic Papers 74 (2): 382–411. https://doi.org/10.1093/oep/gpab021.

@article{MS22,

author = {Pascal Michaillat and Emmanuel Saez},

year = {2022},

title = {An Economical Business-Cycle Model},

journal = {Oxford Economic Papers},

volume = {74},

number = {2},

pages = {382--411},

doi = {https://doi.org/10.1093/oep/gpab021}}

Related material

- Presentation slides

- Working paper (2014) – This version of the paper assumes that the government issues not only bonds but also money. The model provides a microfoundation for the IS-LM model. It is useful to analyze open-market operations and helicopter drops of money.