Abstract

This article develops a model of unemployment fluctuations. The model keeps the architecture of the general-disequilibrium model of Barro and Grossman (1971) but takes a matching approach to the labor and product markets instead of a disequilibrium approach. On the product and labor markets, both price and tightness adjust to equalize supply and demand. Since there are two equilibrium variables but only one equilibrium condition on each market, a price mechanism is needed to select an equilibrium. We focus on two polar mechanisms: fixed prices and competitive prices. When prices are fixed, aggregate demand affects unemployment as follows. An increase in aggregate demand leads firms to find more customers. This reduces the idle time of their employees and thus increases their labor demand. This in turn reduces unemployment. We combine the predictions of the model and empirical measures of product market tightness, labor market tightness, output, and employment to assess the sources of labor market fluctuations in the United States. First, we find that product market tightness and labor market tightness fluctuate a lot, which implies that the fixed-price equilibrium describes the data better than the competitive-price equilibrium. Next, we find that labor market tightness and employment are positively correlated, which suggests that the labor market fluctuations are mostly due to labor demand shocks and not to labor supply or mismatch shocks. Last, we find that product market tightness and output are positively correlated, which suggests that the labor demand shocks mostly reflect aggregate demand shocks and not technology shocks.

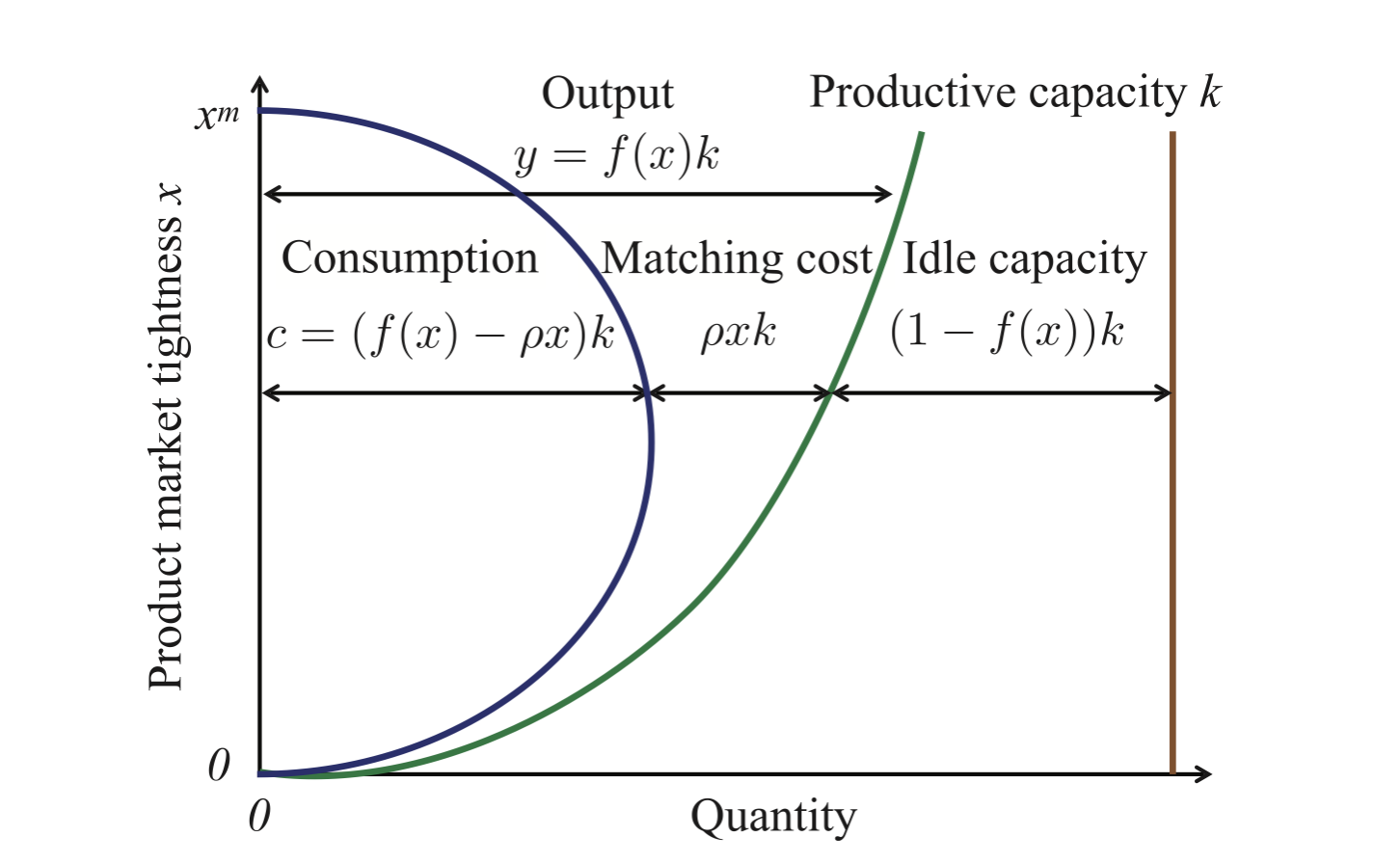

Figure 1: Matching process on the product market

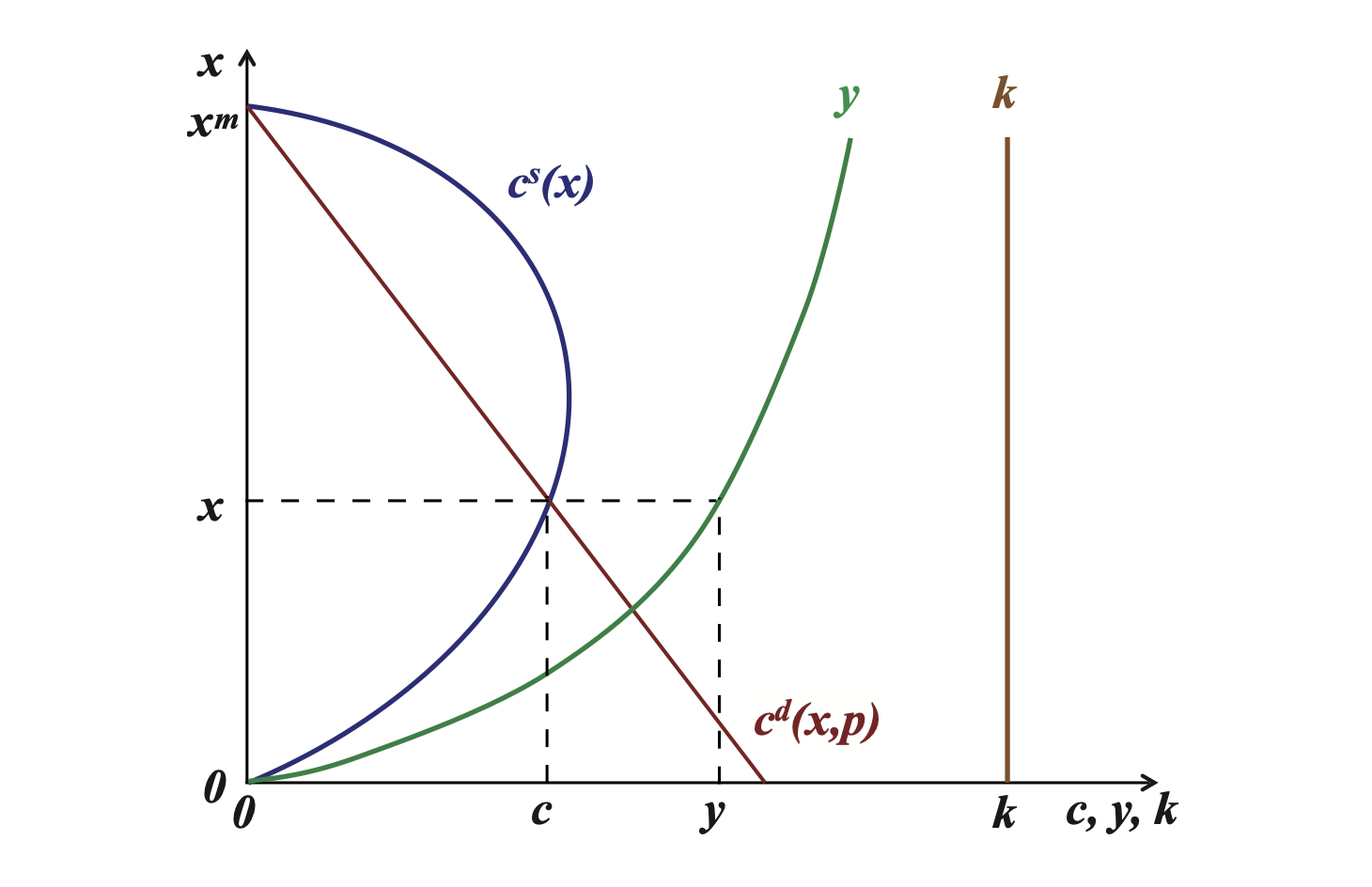

Figure 3A: Aggregate demand and aggregate supply on the product market

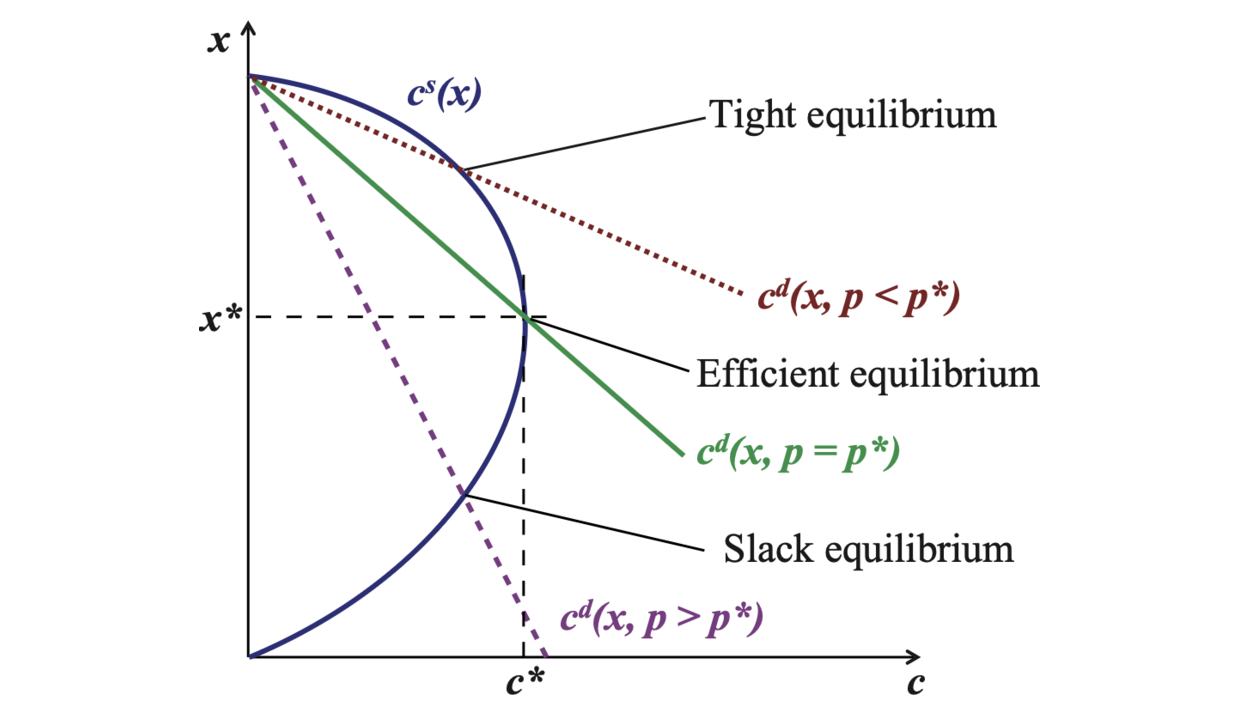

Figure 4: Three regimes on the product market

Citation

Michaillat, Pascal, and Emmanuel Saez. 2015. “Aggregate Demand, Idle Time, and Unemployment.” Quarterly Journal of Economics 130 (2): 507–569. https://doi.org/10.1093/qje/qjv006.

@article{MS15,

author = {Pascal Michaillat and Emmanuel Saez},

year = {2015},

title = {Aggregate Demand, Idle Time, and Unemployment},

journal = {Quarterly Journal of Economics},

volume = {130},

number = {2},

pages = {507--569},

doi = {https://doi.org/10.1093/qje/qjv006}}